mhifoe

-

Posts

411 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by mhifoe

-

In A Crash - How Do People Survive .....

mhifoe replied to Perfectionist's topic in House prices and the economy

Shopping for luxuries is something that will undoubtedly suffer. At my local town centre, Dixons and HMV are far emptier than normal. However Wilkinsons and Poundland are heaving. It's also interesting to note that 2 new pound shops (Huge ones) have opened in the last 6 months. -

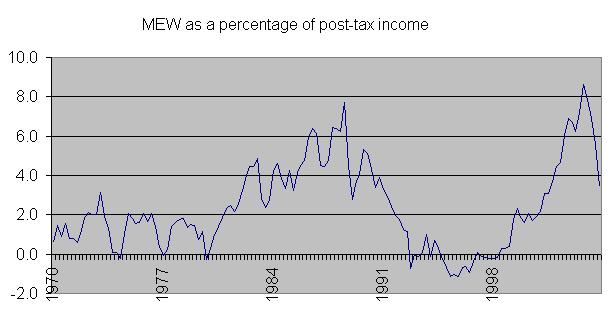

This was also discussed in this thread. Attached is a graph of the data.

-

Here are the latest MEW figures: http://www.bankofengland.co.uk/mfsd/mew/mew.htm 2003 Q4: 16,817 2004 Q1: 15,525 2004 Q2: 13,724 2004 Q3: 11,297 2004 Q4: 6,933 Quarter on quarter change: down 39% Year on year change: down 59% The BOE website also links to a spreadsheet with the figures since 1970.

-

Have any moderators read this thread? The hometrack figures on the front page need updating with this information.

-

Hometrack PDF report That's what we like to see. No mention of the year on year drop in the summary though.

-

Consider higher rate earnings of 1000. Gross: 1000 Inc Tax: 400 EE NI: 10 ER NI: 128 Net: 590 Tax: 538 Therefore higher rate earnings attract 48% tax, leaving you with 52%.

-

I am quite tempted to buy a few gold coins from taxfreegold. The thing that concerns me is how I would go about converting it into cash at some point in the future. Who can I sell the coins to for a good price? Would I be better off investing in a gold fund?

-

I hope that's the case, but I rather expect the revaluation to be used as a money grabbing exercise. The bands will be increased, but I doubt they will go up as much as the valuations. This quote is from Ceredigion council following their rebanding last year: "Initial indications show that approximately 3% of households in Ceredigion will receive a reduction in their band, 58% will remain on the same band, and 38% will be subject to an increase in their band. The majority of the increases will be one band only, although there are some subject to a two band increase and a smaller number subject to at least a three band increase.

-

Borrowing 7 times income is absurd, unless you are happy to live in poverty or go bankrupt following a small rise in rates. Let us consider someone on 20k borrowing 7 times salary. The figure in brackets represents the percentage of take home pay consumed. Net income: 1275 IR: IO: RP: 6%: 700 (55%) : 902 (71%) 8%: 933 (73%) : 1081 (85%) 10%: 1167 (92%) : 1272 (100%) Do you really consider these figures affordable?

-

Ftbs & Young Starter Families Are Trash To Labour

mhifoe replied to right_freds_dead's topic in House prices and the economy

Indeed. Let us consider the previous poster who said that someone on 50k gets 40 quid a month of benefits. Monthly salary: 4167 Income tax: 1017 Employee NI: 263 Employer NI: 483 Total tax: 1763 Therefore the 40 quid is hardly coming out of someone elses pocket. -

What about employers NI contributions? The government may like to pretend it isn't a tax on income but it is. Low rate: Income tax: 22% employee NI: 11% employer NI: 13% Total: 46% High rate: Income tax: 40% employee NI: 1% employer NI: 13% Total: 54%

-

Double Digit Council Tax Rises Next Year?

mhifoe replied to OnlyMe's topic in House prices and the economy

The Government has the power to cap council tax rises and this year it threatened to do so if any council attempted an increase of more than 5%. Also, as Derek mentions the council tax revaluation is likely to push up many people's bills. One of the Welsh revaluations resulted in 38% of properties being pushed into a higher band. Only 3% of properties went down a band. -

That's an interesting interpretation of affordability. Let us consider a 7x income multiple on an income of £20k. Post tax income: 1262 140k @5.5% IO: 642 140k @5.5% RP: 860 So without further rate increases this mortgage would consume over 50% of income interest only and almost 70% repayment. Also, what would happen if interest rates were to rise slightly (examples are interest only? 6%: 700 (55% of income) 7%: 817 (65% of income) 8%: 934 (74% of income)

-

FTBs Section: Living at home/rented/shared etc: Rent a 2 bed house When you plan to buy, or if: Hopefully in 2-3 years (if there is a fall in prices of 30%) Rental Costs: 500 pcm Rent going down or up: Rent unchanged since moving in 2 years ago. The flat we lived in previously was with the same landlord. He never increased the rent in the 4 years we lived there. Do you think the market will continue to fall: Yes.

-

Channel 4 news had a breakdown of the effect on different family types of Labour's changes. A couple, both unemployed with children are 25 pounds a week better off. A couple, both employed without children are 25 pounds a week worse off. Basically, anyone who actually works for a living is worse off.

-

Type 43: Older people, rented terraces (1.89% of the population live in this ACORN type) Likely Characteristics This type is found predominantly in northern English towns such as Oldham, Salford, Liverpool, Huddersfield and Gateshead, as well as in Belfast and some towns in the south including Basildon. Family Income : Low Interest in current affairs : Medium Housing - with Mortgage : Low Educated - to degree : Low Couples with Children : Low Have satellite TV : Medium This type has a high proportion of older people, particularly those over 75, living in rented terraced housing. There are fewer families with young children in these neighbourhoods, although there are some single parents. Single person households are most common and many are pensioners. Most residents live in small terraced houses, with only two or three bedrooms. Some live in flats, mostly low rise purpose built. There is a higher proportion of residents renting compared to the UK as a whole. Many rent from private landlords but local authority and housing association property is also important. There is a high level of re-mortgaging among those who are buying their properties. Those in work tend to be shopworkers or are employed in manual and factory jobs. However, unemployment is 40% above the national average and long term illness 60% higher than the UK as a whole. Car ownership is low and public transport, cycling and walking tend to be the main modes of travel. Incomes are low and there is little scope for savings and investments. Take up of credit cards is low, but some find it hard to manage and levels of debt are above average relative to income. Leisure interests include angling, racing, bingo, watching cable TV, listening to music and going to the pub. Popular newspapers are the Daily Mirror, Daily Star, Daily Sport and The Sun.

-

I was interested to note that today's BBC Article about the land registry figures makes no mention at all of the quarter on quarter drop in prices. Instead they are remarking on a slowdown in year on year figures. Are they taking the piss?

-

Insanity Continues ? - 13 Visits 3 Notes

mhifoe replied to judas's topic in House prices and the economy

Jesus is a very rare name in the UK. I have never met anyone with that name. Therefore whenever someone mentions Jesus people immediately this of that friendly chap who died approximately 2000 years ago. The first time I saw your username I thought it was chosen to facilitate jokes about religion. Don't worry about it, everyone will stop making jokes after a few days when they realise it's your actual name. -

I drive old cars which cost under £500. One thing to note is that large non-prestige cars (Scorpios, Omegas) are very good value. There is a lot of interest in small cars for young drivers, which tend to inflate the price. For example, a 10 year old Nova or Clio will cost more that a top spec Vectra or Mondeo. There is also less of a problem with rust these days. Major manufacturers started zinc coating their chassis 10-12 years ago. Before that a 10 year old car could need significant welding, but now they are rust free.

-

Blitz On Estate Agents Bogus Sold Boards

mhifoe replied to jpjh's topic in House prices and the economy

An estate agent attached a 'sold' board to a lampost in my street, probably so it was more visible from the main road. It annoyed me so I cut it down. -

Income tax is only 22%. However, national insurance contributions are 23.8% (11% employee, 12.8% employer) Indeed we do get free healthcare, but I'd rather see money spent on education than the ODPM*. *Office of the Deputy Prime Minister

-

US students do pay a large amount for their education, but then they will enjoy a lower tax environment when they graduate. The average UK graduate can look forward to a basic tax rate of 45% including employee and employer NI contributions. Not to mention council tax. As a country with a farily high tax rate we should expect something for our money.

-

In the programme, the bank was insisting on very expensive PPI to people who wouldn't be able to claim on it. Basically they were selling PPI to get the commission without any concern for whether the loan could be repaid. They lent nearly 30 grand (including 6k of PPI) to an unemployed man whose loan repayments exceeded his benefits. If your partner is in temporary work it is unlikely that PPI would be suitable. It sounds like they are just after commission. There is some information on their website: http://www.bbc.co.uk/realstory You can also watch the programme again from there. Good luck.

-

The worst ever figure was -66% in 1990. The Motley Fool is currently running a poll on when this record will be broken. http://boards.fool.co.uk/Message.asp?mid=8997409

-

You are comparing 11k in 1996 with average earnings in 2004. This is not a fair comparison as average earnings in 1996 were £18k. Your example shows that affordability has remained relatively stable for someone whose salary has almost doubled in real terms. Harldy indicative of a sustainable trend is it?