captainb

-

Posts

4,533 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Posts posted by captainb

-

-

Could be a typo and 1,250 a year.

It's also a short lease under 80 years, which should be more of a red flag and hence the price.

-

Why do people transact internationally in USD rather than local currencies in sub Saharan Africa.. erm...

-

1 minute ago, 2buyornot2buy said:

The inlaws are thinking of selling and downsizing at the moment. I said I'd arrange a few calls with local EAs to get a very general idea on price. Spoke to 3 EAs and got into a bit of a conversation about rates with 2 saying the inlaws would buy something smaller and stick the rest in an account for a few years and supplement the income by about 25k.

Both EAs were absolutely adamant rates will drop before year end. One thought they'd be back to "normal" quick snap... this is what they believe.

So I'd hold off. This is going to be long and drawn out over years. Not months.

Given they pay their own mortgage by volume of housing transactions they are hardly ever going to say sit tight.

-

You can always offer. They can say no thanks.

No harm to either side aside from the 5 mins it takes.

-

Meh. Relative to wages makes sense to adjust; adjusting to say it's "cheaper" as price of cheese has skyrocketed is hardly relevant nor helps anyone buy.

-

5 minutes ago, nero120 said:

Sorry you think migrants arriving on boats are paying sky high BTL rents?! LOL!

As interest rates go up, zombies companies go bust, people lose their jobs, those wanna-be middle classers that were in London to "find their fortune" will either become OOs or GTFO of London.

Why can't people accept the fact that the era of cheap money is OVER.

No I don't think that but you seem to be under the illusion that most migrants arrive in small boats...

Good luck waiting for the rental collapse.

-

4 minutes ago, nero120 said:

BTLers are dumping, private equity WILL NOT be buyers, renters become OOs, rental demand falls as does supply, less BTL means rents do not need to aggressively increase to match interest rates, it's really not that hard.

Cool. And in this scenario, there's no increase in rental demand from population growth right? Or people giving up on expensive mortgages and downsizing to rent?

I'm going to make a bizarre prediction that new rental supply will continue to suck in increased % of rising wages as supply dwindles against worsening demand. Just like it has over the last couple of years......

Of course it could be solved by the state building an appropriate level of housing to satisfy demand at the lower end rather than HMO etc. Sadly they won't.

-

3 minutes ago, nero120 said:

HAHAHAHAHA!!!

You seriously think private equity is going to keep london property prices inflated when they can now get decent yields in MMFs for zero risk (which will increase as interest rates continue to increase)?! Why TF would any investor choose to tie up their capital in a depreciating asset whose price is dropping like a stone?!

What curious ideas some people have!

Nope but they will push to keep rents high to cover those debts.

Which was your original bizarre point... That somehow massive reduction in supply will reduce rents (in the absence of new builds)

-

1 minute ago, nero120 said:

Who would they be renting from? The same BTLers that are currently being lined up for the slaughter? A landlord with no mortgage to pay is not so concerned with squeezing their tenants for all the rent they can get.

Rents will fall as the BTL abomination is wiped from the face of this earth over the coming year.

Given replacement of the BTL bro is an private equity backed bro, rather than dorris with no mortgage wouldn't bet on it

Check out the prices on them.

-

"Current rental income of £110,976 per annum."

If it goes for asking £2.5m that's a gross yield of under 5%, not sure I'd call that a great sell off bargain.

More likely a lot of the flats are tiny studios with that level of rent.

-

12 minutes ago, hotblack42 said:

Kensington & Chelsea? There's huge national and international demand to live in that borough and yet there are 23,625 council tax arrears cases?

Surely it would make more sense to lift and shift these people, write off their debts and allow wealthy and well paid council tax payers to displace them? Anyone living in that location who can't get a well paid job can't have much to offer, or am I missing something?

There's quite a few large council owned sites (think around Grenfell and others), not all South ken old money.

Additionally you will probably find a load are people too posh to open the mail and end up paying with the fine once the secretary finally gets the call that otherwise they goto court.

-

3 hours ago, The Angry Capitalist said:

Yes.

They are scum.

The rich will be the last to get their pockets emptied.

That being said there is more potential tax to be gained from the general population than the richest.

Also, the richest will just emigrate if the government tries chasing them. They will be the last to get shaken.

If they do start trying to tax the rich more you know the government is at the furthest it can go without going into communism or outright socialism. It's desperate times when they start to try taxing the top 5% -10%

At that point they either go down the serfdom road or start to shrink and reduce spending significantly.

Those people are better off not showing up to court. No judge can order a warrant to arrest them.

Worst case scenario they get bailiffs coming to their door but just don't pay them.

They are not obligated to pay anything. Council tax is voluntary. Might be stressful dealing with the bailiffs but if it means the councils get starved of revenue to pay all their big pensions then so be it.

On the off chance someone takes this seriously, no that's really not the case nor a good idea if you are indeed liable (i.e living in the property on an AST or it's owner in a tenants absence).

-

Tower Hamlets is in the mix as well.

Lots of unfunded promises by a mayor previously convicted of corruption

-

If you want exposure to a property asset without the hassle of dealing with tenants etc there is always warehouse reits. Something like BBOX or SHED, put in an ISA and the dividend income is tax free.

Not financial advice

-

There never was going to be a trade deal with the states as stated continuingly by those with any knowledge whatsoever on the matter from 2015 onwards. Best route in would be via a 3rd party deal like CPTPP

Still awaiting that brexit dividend.

-

5 minutes ago, Wurzel Of Highbridge said:

I'm surprised that nobody has brought up the shockingly high prices in ASDA! It's a matter worthy of it's own topic.

I've refused to go back in there. They're playing a game where they stock the minimum quantity of own brnaded goods, so when they run out people have to buy the vastly overpriced branded goods.

One small example, nearly £5/kg for chips?

Similar product in ALDI

I hear you cry, that Asda will also have a cheaper own branded product - Yes they will, but they are deliberately stocking a small quantity to keep the appearance of low prices. Unless you go in at 8 am you won't find any stock!

They even went as far as limiting 3 of any value product to customers - they seem to have dropped this after bad publicity.

3 x cans of beans is enough for your family of 6 sir!

Asda need to be pay for the 2billion or so of debt they have been laden with.

Like supporting man utd, you pay extra, and the store/stadium is falling apart as all the money goes to paying off the owners loans

-

52 minutes ago, regprentice said:

We've been building houses slower than weve been importing "talent" for years. theres also a shortage of houses generally and i read a few days ago it would take 4.5 million houses to redress the balance across the UK.

if you start with a deficit of 4.5 million houses, continue to import 600k people net and build 1mn houses a year then it will be 2033 before there are enough houses to meet our current need and the increased need through immigration alone. if migration and house building continue at their current level then that 4.2mn shortfall gets worse by 420,000 houses every single year

For the last two years running we have built almost exactly 420,000 fewer houses than the figure for net migration that year. Rishi Sunak hailed last year as a record breaking year for house building but only built only 173,000 houses in England. link . it seems physically impossible that we could ramp up to 1mn houses a year.

Also gap between where houses are built (all over) and where migrants typically want to live (cities). Hence Manchester, London etc gone Tonto.

-

6 minutes ago, wighty said:

Iht allowances are too complicated.

The 7 year pet rule must be almost impossible to administer by HMRC.

I'd suggest HMRC rely on people fessing up to gifts unless it's £millions.

People give HMRC far too much credit based around the odd unlucky vat visit. Where normally they just ask to see a few invoices anyway.

See huge amounts of vat carrosel fraud, bounce back loan payments to directors, most landlords don't declare the income, "side hussles" etc etc etc

They rely on honestly but in a pure cost / benefit analysis you'd be better off just ignoring them.

-

10 minutes ago, Unmoderated said:

Fully agreed. High end stuff it's hard to find anywhere else. Generic labelled stuff it's probably another level of WAT (Waitrose Added Tax) on the VAT.

Since it's walking distance though I must admit I use them more than I should. Also have an Inspire award scheme at work (points given for good jobs and then converted to prizes including Waitrose/John Lewis Vouchers) so I will take a £100 voucher down there and restock whisky cabinet. When they have stuff on offer it's actually good value tbf, wines too. As you correctly observe though their standard pricing is simply there to keep the riffraff in Tescos I think.

The 25% off any 6 bottles of wine in Waitrose is a good shout for stock up/voucher use as long as you purchase wines that were decent/reasonably priced at full

-

5 minutes ago, clarkey said:

Still doesnt make the secondary taxes right though.

We still have the landed gentry , royal family and hangers on, dukes and soforth. I bet they don't pay IHT so its just for the plebs really. Id argue most of the Downton type landed gentry disappeared as staff found better jobs / went off to fight in wars / labour saving devices meant they did'nt need the staff

Not sure what you mean by secondary taxes.. you would just have income tax set very high and that's it? My point is they are everywhere so claiming that inheritance tax is somehow an outlier by being one is misleading.

I'd also get rid of the monarchy in a heartbeat but that's another story. Not really the downtown Abbey types sons had to sell the estates the pay the inheritance taxes and the family silver.

-

10 minutes ago, clarkey said:

Most inheritances are built up in savings (from wages) and or property (from paying the mortgage)that has already been taxed once so that’s unfair, thus also discourages saving

I've been taxed on my salary, if I goto a pub im taxed a second time beer duty, vat etc.

Secondary taxation is always there.

Not sure I want to go back to the landed gentry crap of the Edwardians. Noting with a £1m allowance it's only that set who it will benefit.

-

8 minutes ago, fellow said:

The global recession begins?

Eurozone falls into recession

Ireland GDP is meaningless as it's so distorted by large internationals funneling profits through there for tax reasons.

I.e. it has very little to do with the Irish economy and a lot to do with how apple and Pfizer etc decide to structure their IP this qr

-

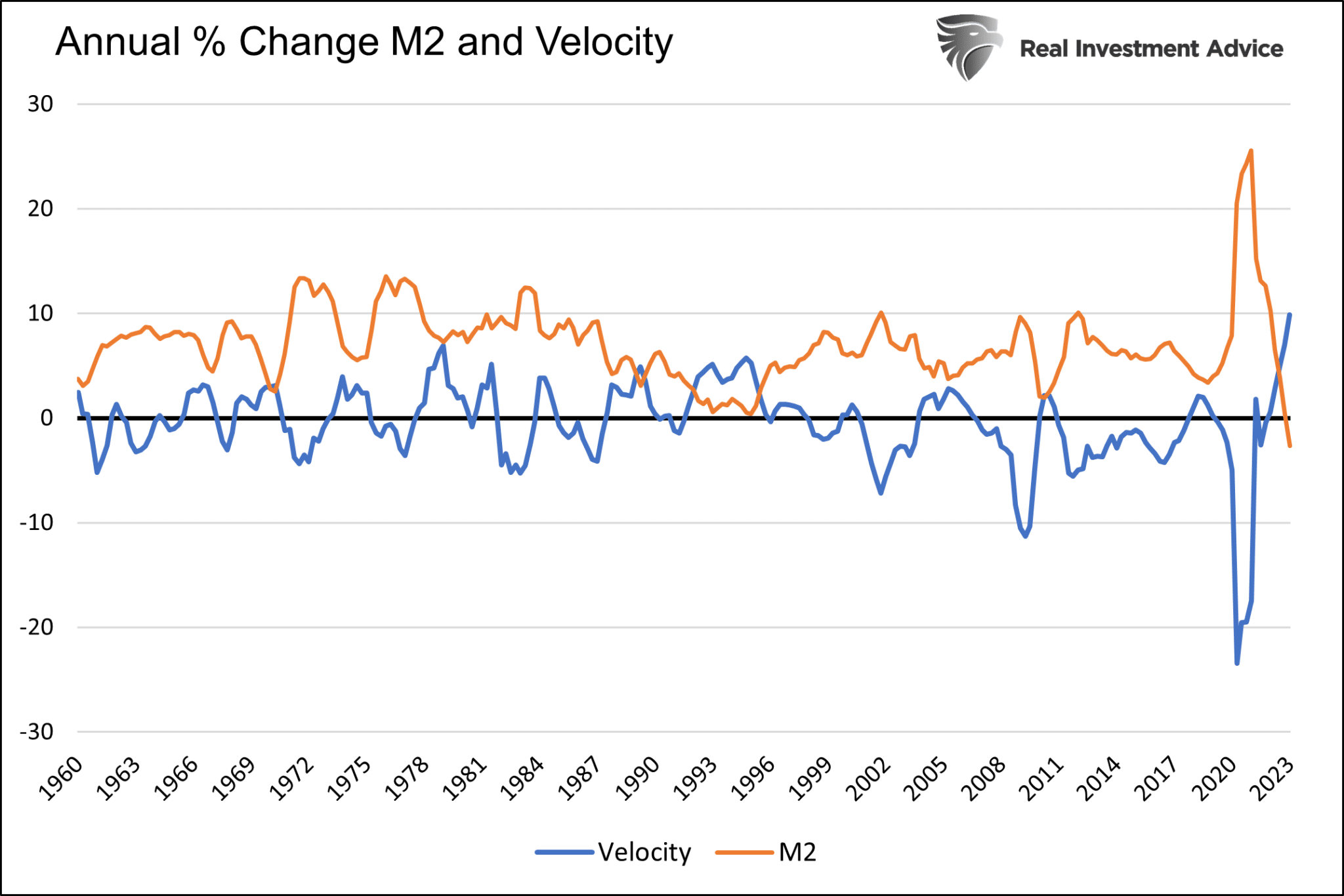

1 minute ago, slawek said:

No. Inflation will be sticky because of increasing money velocity. With high inflation people are more willing to spend money than keep it in a bank account. It is an inverse process to one which happens during a deflation period when people hoard money, making the crisis worse.

Many years of credit expansions and QE created lots of money, which didn't cause inflation because most of it lied idle in bank accounts. Now this wall of money has been activated. It will take higher rates and some pain to stop this process, even with the money stock going down.

That and covid. Loads of people who saved though not going out on holiday etc are suddenly realising life is short and they should definitely go on holiday etc this year.

-

19 minutes ago, Mikhail Liebenstein said:

Probably some stockbrokers once upon a time, but the successful ones were likely in other Surrey towns, like Weybridge.

Cobham and around there are same council I believe. Odd helicopter pad round that way

In one week the situation has deteriorated

in House prices and the economy

Posted

Because the risk as calculated by the banks modelling doesn't materially shift between the those levels assuming acceptance.

At a guess, if you pass the credit check for a large mortgage in GBP you are screwed whether you borrowed 80% of the LTV or 60% if you lose your job

Conversely in either scenario the bank expects to get the full amount back at auction.