fuzzy_bear

-

Posts

110 -

Joined

-

Last visited

About fuzzy_bear

-

Rank

Newbie

")

-

If inflation falls to zero tomorrow, prices simply stay at the current elevated prices. Sounds like you're really hoping for deflation which isn't going to happen. Equally, with cost of living as it is, labourers are unlikely to settle for a pay-cut this year or next.

-

Are you keeping your gas under control?

fuzzy_bear replied to Mikhail Liebenstein's topic in House prices and the economy

Live up North on a hillside. Snows more than most of rest of UK. Out at work during the day so heating off. Thermostat at 18 when home. 16 overnight. 40 kWh/day in winter months 20 kWh/day in warmer months Perfectly comfortable The odd time the temp hits 25 in Summer I find it really uncomfortable - its difficult to sleep in that heat. Can't imagine heating the house to that temperature deliberately. -

Time to turn off the crypto miners?

-

BoE predictions for Thrusday?

fuzzy_bear replied to henry the king's topic in House prices and the economy

Savings rather than mortgage I assume? 😂 Unlikely there will be a significant uplift in bank rates as this has been priced in for a few months now -

BoE predictions for Thrusday?

fuzzy_bear replied to henry the king's topic in House prices and the economy

Of those three, Mann voted for 0.75% increase -

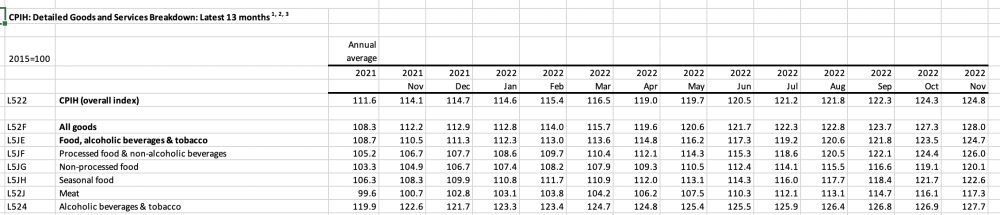

Data is all there in ONS - category & even individual items

-

The BBC is sick - great time to not have a TV

fuzzy_bear replied to athom's topic in House prices and the economy

So you don't watch/listen/read the BBC but you start a thread with a linked article. . . from the BBC? Without this thread I doubt most of us would have seen this -

It is addressed. Reality is that the UK housing market is much less exposed to interest rate rises & household debt than many countries. How things play out in these other countries will give us some idea of what might happen in UK

-

103,930 transactions were recorded in September in UK

-

You do know that your debt obligations travel with you? To the USA where umm. . . 30-40 year mortgages are standard

-

looks like the BoE has lost all credibility

fuzzy_bear replied to TheCountOfNowhere's topic in House prices and the economy

Failure to raise rates quickly enough in UK is a big part of the reason for the pound's weakness Pound would likely strengthen in response to a higher than expected rate rise (e.g. >0.5%) -

Not sure how you work that out Average mortgage in the UK is around £140,000 (Q4 2021) 2% = £593/month 3% = £663/month

-

Has Your DC Pension Lost Money?

fuzzy_bear replied to Greater Fool's topic in House prices and the economy

If you're cheering on a house price crash, you are hoping for economic conditions that will adversely affect your pension investments. -

Where will the growth come from?

fuzzy_bear replied to winkie's topic in House prices and the economy

"bin" infrastructure projects to promote economic growth? Interesting economic theory there -

Lots of Telegraph links on here & every one behind a paywall - does everyone else have a Telegraph subscription?? Can't believe people pay money for that rag