Wolfie84

-

Posts

48 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by Wolfie84

-

Foxtons Share Price And The Housing Market - Merged

Wolfie84 replied to jasonpistol's topic in House prices and the economy

Looking forward to seeing their Q3 report. Should be out by the end of the month. If they last that long... -

Why are house prices starting to fall ?

Wolfie84 replied to TheCountOfNowhere's topic in House prices and the economy

Rather than BTL running for the exits, I think it's more that they're no longer buying. Leaves OO with less spending power (as repayment mortgages rather than interest only). Also leaves plenty more for scope for bigger drivers of falls to kick in (BTL tax changes, forcing sales. Interest rate hikes having same effect etc) -

Oh, and if you can't get anyone to rent it out, just drop the price, innit 03/07/2017, Price changed: from '£1,550 pcm' to '£1,400 pcm' http://www.rightmove.co.uk/property-to-rent/property-67196177.html And chuck it up for sale, innit http://www.rightmove.co.uk/property-for-sale/property-67377356.html

-

http://www.rightmove.co.uk/property-for-sale/property-67394846.html Got the Receivers in to sell this. One to watch?

-

RIP High Street Estate Agencies

Wolfie84 replied to Wolfie84's topic in House prices and the economy

You're right. You never see an old estate agent do you? Turns out it is possible to die from shame (with due credit to Al Murray) -

Is Prime London Crashing? - Merged Threads

Wolfie84 replied to Damik's topic in House prices and the economy

They're probably just correcting a typo from 1,910,000 to 1,190,000, I'm afraid. Imagine the embarrassment though when they realise they still need to knock a zero off the end to make it right. -

Land Reg May 2017 (data for March) -0.6% MoM

Wolfie84 replied to rantnrave's topic in House prices and the economy

The first one was filtered down to searches from England (I think). Yours looks to be worldwide? Are there any (easy to use/process) sources showing the average length of time since previous sale within Land Registry data? So, for all sales in March 2017, what was the average previous sale date. And is this a shorter or longer time frame from previous months/years. I'm not sure what it will show, but think it could be interesting!

-

I'm always interested in tables like this. To me it begs the question of how far house prices would need to drop so that BTL would make the same money as it does now. So I've run the numbers. The first two columns in the table below, recreate the first and last table from above. The third shows 'net profit after tax' being back to the initial £1,680. To make the same profit, the mortgage interest (and therefore house price) need to fall. With my calcs, prices drop 25% to £262,500 (see below) Now, this ignores the upfront costs and any changes in interest rates, which maverick73's table shows would make the situation worse for the landlord. Hopefully, it should be obvious that these would have a further crippling effect on house prices. The other point to make is that this has assumed constant rental income. The numbers above show that the marginal buyer is less likely to be BTL as the profits don't make sense for them at these prices. So if prices fall, this would encourage those in the PRS to shift to OO. These are more likely to be richer renters (as house prices are still high), so those remaining in the PRS will be poorer, on average, than currently is the case. Because of this shift, constant rental income appears, err, optimistic from the point of view of a BTLer.

-

Is Prime London Crashing? - Merged Threads

Wolfie84 replied to Damik's topic in House prices and the economy

It's also where the estate agents that I've shown are closing down in my thread below were based. -

RIP High Street Estate Agencies

Wolfie84 replied to Wolfie84's topic in House prices and the economy

Roses are red Violets are blue This agency's gone Boo-f*cking-hoo

-

Is Prime London Crashing? - Merged Threads

Wolfie84 replied to Damik's topic in House prices and the economy

Thanks a lot for all the posts on this (and other) threads with this info. Like others on here, I'm finding this incredibly interesting. It's maybe a bit of a naive question, but to what extent could the recent falls in some of these areas be as a result of changes to the profiles of housing stock in the area? Could all the 2 bed flats that are being thrown up all across London be skewing the data as it leaves larger houses as a proportionally smaller chunk of sales? -

Some of the debt forgiveness is written in to the T&Cs, I suppose. The stuff below is from the help to buy site. I guess being on the hook for these losses is another reason the govt won't remove any props :-( https://www.helptobuylondon.co.uk/docs/default-source/default-document-library/help-to-buy-buyers-guide-oct-16-v1016.pdf?sfvrsn=0

-

I think this is nailed on

-

Is Prime London Crashing? - Merged Threads

Wolfie84 replied to Damik's topic in House prices and the economy

Come on, just look at the "Reasons to Invest" "Potentially high level of capital growth""Great anticipated rental yield" Here’s a couple more you might enjoy. http://www.rightmove.co.uk/new-homes-for-sale/property-46792671.html Off place re-sale below contract price! BARGAIN! http://www.rightmove.co.uk/new-homes-for-sale/property-55175312.html Asking price down £80k this year, completion due this year. -

Oh, indeed. I think all of the factors like this are massively shooting the "purchasing power" of BTL out of the market. Which just leaves OO (and overseas in some places) buyers in the market. Prices are way to high for OO, so transactions have fallen off a cliff. Just need a few BTL forced sales to OO to kick start the falls and then it'll all collapse in on itself. An interest rate rise to counter inflation from the fall in the £ should do the trick, but I'm not holding my breath on it happening any time soon

-

Okay, so here's a first stab at this. There's a big block of flats near me which have a load of essentially identical units, so I can see what the current sale and rental prices are. At the moment, these are going at £270k to buy and £1k pcm rent (conveniently £12k p/a) Current World With 75% LTV, we're looking at a £200k mortgage. A 2% IR on that, means annual mortgage payments of £4k. Current Tax Bill (if on higher rate) is £12k - £4k = £8k at 40% = £3.2k So I think(...) we're looking at £12k - £3.2k - £4k = £4.8k per annum to cover maintenance costs and "profit". New World The tax bill becomes £12k at 40% = £4.8k. This is £1.6k more than before, so my thinking is that a BTLer would have to keep paying the same maintenance costs and would want to keep the same "profit" the thing that has to drop is the mortgage payments. So mortgage payments drop from £4k to £2.4k. At 2% Interest Rates, this would imply a mortgage of £120k and total price of £160k. I appreciate the back of the fag packet maths on this, but it would imply these changes would drop house prices by 40% doesn't it? Obviously there are limitations to this analysis: At lower prices, a landlord might accept a lower nominal "profit". With my sums, as prices lower, yield goes up as I'm assuming a fixed amount for "profit". This would dampen the HPC effect At lower prices, a landlord might decrease the LTV, reducing the level of interest paid on the mortgage. Again, this would dampen the HPC effect. At lower prices, owner occupation becomes more viable for people, reducing rental demand. This effect would lower rental income on the property, meaning the landlord would have to reduce their mortgage payments even more to maintain the profit. This would increase the HPC (Increasing to Interest Rates to 4%, gives a £60k mortgage and £80k price?)

-

We are where we are though and clearly future policy changes can deter BTL more. Going back to my original point though, around where I live we got to a stage (at least pre-stamp duty going up on 2nd homes) where BTLers were happy chucking £500k at properties which would generate £1,500 pcm. I'm sure some of this is based on an HPI forever mantra, but there is also the question of what it returns each year. The changes that are coming are going to change the way these annual returns play out, so judge the size of a potential HPC it seems relevant to ask how much a BTLer might chuck at a property generating the same rent, after the tax/regulations have changed. After that, we can have an argument about how much more needs to be done to clobber BTL :-) Sadly though, I don't know what maths would be involved to work out the answer to my question :-(

-

I’ve been thinking about how the BTL market will change and how this then feeds back into overall house prices, but struggling with the maths. Perhaps someone one here could lay things out to help my thinking. The overall hypothesis is that prior to “BTL changes” (see below) a BTLer could borrow £x and make a certain yield, but after the changes they could only borrow £x-£y to make the same yield. Following on from this, crucially, I’m wondering whether £x is more than an OO could afford and £x-£y is less :-) The key BTL changes I’m thinking of are: Changes to tax relief (no more offsetting of mortgage interest against rent) Changes to bank lending (rent must (I think) cover 145% of repayments vs 125%) To get towards this, I think I need to have a few fixed factors to start to get a feel for what might happen. So my first question is: For a fixed rental income of £1,500 pcm, how much would I be able to pay to get a, say, 5% yield on a BTL property from this rent. I imagine that I need to assume a fixed LTV (say 75%?). I also want to assume that the BTLer is a higher rate tax payer, so they get the full clobbering from the tax changes :-) The next question is: Same scenario as above, but with 2% added to the mortgage interest payments. I appreciate that this might be a little too simplistic (particularly with rent being fixed), but I’m really interested in knowing how I could go about working out these kind of scenarios, ultimately to see how far prices might fall as BTL landlords leave the market. Thanks in advance for any help on this!

-

The first one. "Brain Cox are delighted to offer..."

-

RIP High Street Estate Agencies

Wolfie84 replied to Wolfie84's topic in House prices and the economy

"Will the Internet Replace Estate Agents?" asks the Samuel Estates website. They've not updated the article to show a picture of their former office yet. Really, i think this is just showing how far transactions have dried up. This office ran the sales for a new build block of flats next door (you can see some 'sold' signs in the window), but they're not shifting as they're massively over-priced. Overseas buyers can't be buying any more. BTL landlords can't be buying any more. And the flats here would be double digit multiples of income for owner occupiers so they can't buy either

-

Premium Listing

-

Here we shall commemorate the passing of estate agent offices, as they close down and pass into productive uses that benefit society. A selection that i collected on my way to work today: This former Haart office moved on around 6 months ago, I reckon. Look at the haartless way the the signage has been painted over to hide the fact that this was once an estate agent. But I know… You know… We all know… This branch achieved a google reviews rating of 2.2/5, making it one of the best rated estate agents in the area. Reviewers commented that “this is essentially a small-time cowboy operation with extortionate fees” and “This 'company' is absolutely the most unprofessional and incompetent establishment I've ever come across”. Such high praise was still not enough to save it from closure. Perhaps customers will visit their other branch just up the road… …nope, sadly this one’s shut down too. Helpfully, the sign on the door tells customers that they’ve “relocated” to their existing office in Brixton. At first glance this seems like it’s open, with ads still in the window. The more observant among us will notice though that no properties are shown in them and there is a dearth of office furniture inside. A sad sight to see. The irony of a “To Let” sign being placed on a shut down estate agent shouldn’t be lost on anyone. Like a BTL landlord, buying an OO house and creating his own demand, the closure of an estate agent’s offices is good news for retail letting agencies everywhere.

-

Halifax +1.7% MOM +6.5% YOY

Wolfie84 replied to crashmonitor's topic in House prices and the economy

So demanding... ;-)

-

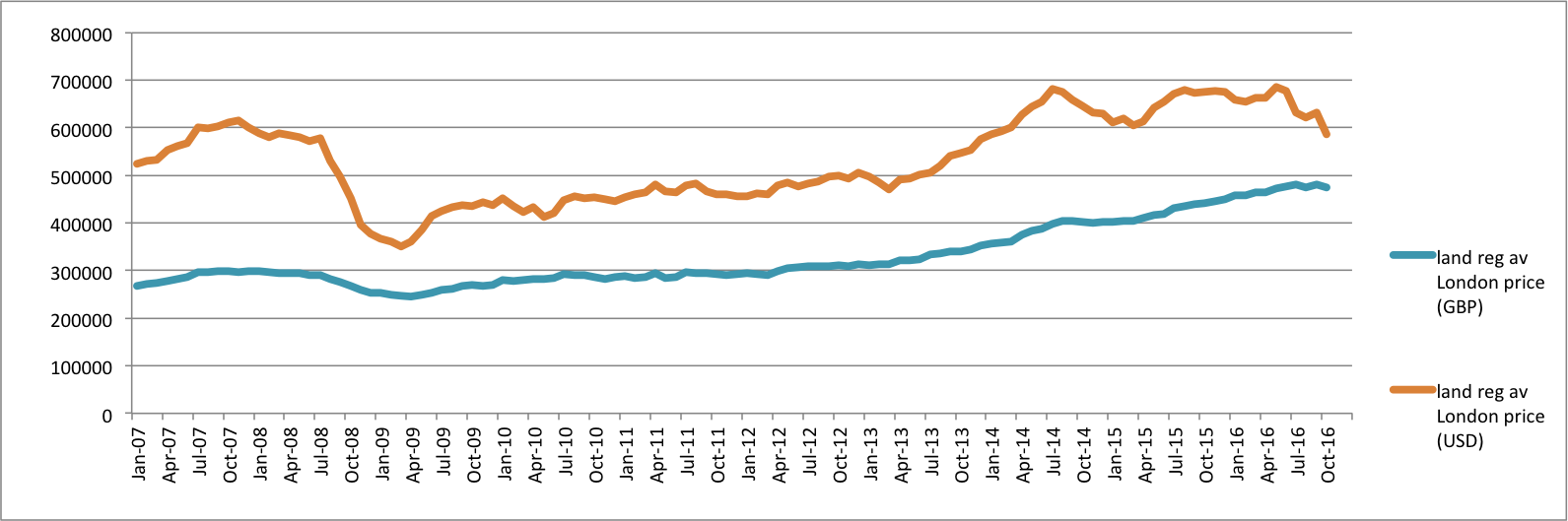

Halifax +1.7% MOM +6.5% YOY

Wolfie84 replied to crashmonitor's topic in House prices and the economy

Here it is from 2007, based on land registry prices

-

Is Property bee working for you ?

Wolfie84 replied to TheCountOfNowhere's topic in House prices and the economy

A new version has been released and it all looks to be back up and running again as normal ?