camem'

-

Posts

372 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by camem'

-

If I've read this right, you can pick your moment in the next 10 years to get your house valued and pay off your 25% loan, but then keep the house until it (maybe) regains value later. So in the case of negative equity, Crest seem to be offering to take 25% of the hit (they get less back from their loan), even if you don't actually crystallise it by moving. Obviously the new build flats they're attaching this to are still comically overvalued, so it's a bit academic, but isn't this actually quite useful if you're going to stay in your house, ahem, for the long term, and think you can pick the 'low' to pay off your loan ?

-

Methinks that affordability one has got some way to fall. Did anyone else see Ken Clarke on some news programme say 'it's easy to get a house these days' ? Lost my vote for how amazingly out of touch that was, not that he's running for anything

-

Gosh, I just made lots of money betting the £ would fall Unfortunately of course, I made it in £

-

Hurray! Just Seen My First Real Price Cut...

camem' replied to sealaw2000's topic in House prices and the economy

how far above sea level is it ? I can't help wondering if you have offered far too much and if you wait 200 months the property will be yours for £12k. -

Lenders Rushing To Seek Repossessions

camem' replied to Weeble's topic in House prices and the economy

New labia same old thighs -

Yeah but you can't live in oil. And it's good for the environment if it costs a lot. Anyway this isn't speculation, it's all about immigration on a crowded island, supply and demand and all that, innit. [here's a graph just in case]

-

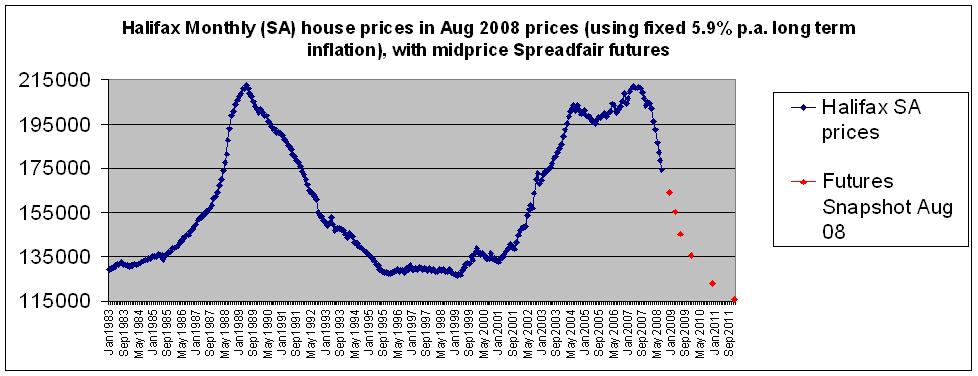

The Inflation Adjusted House Price Graph (1983-2008)

camem' replied to camem''s topic in House prices and the economy

they are, it's just i've applied a different level of inflation to theirs so that the peaks and troughs this time round can be compared to the 90's in today's money. If i did the same to nationwide it would look like this too -

Here's that there graph again. The 2011 future price is down to 107,000 in today's money. Like someone said last time, those futures look oversold If they are, it does look rather like we're halfway through (does that mean I agree with an estate agent ? )

-

How Much Have You Lost On Your Pension Plan?

camem' replied to OLDFTB's topic in House prices and the economy

Checked last Thursday. Lost all of the last 5 years growth in the last 4 weeks to go back to 3% p.a. average since inception (on the 50% that was in the 'opportunity' fund). The 'safe' half 3.5% p.a. Advisor said not to change funds now as it would consolidate the losses... (and then we had Friday...) -

In 20 Years Time People Will Claim They Were Here With Us

camem' replied to a topic in House prices and the economy

which HPC 'character' referred to himself in the third person and invited people to smell what he was cooking ? say 'hope that helps' a lot and see who gets it ? on a related 'we always knew this would happen' note, my 70-odd parents just suggested (for the first time in several years) that it might not be the best time to buy a house, and said this had been obvious for, er, several years. [Result!] -

So I'm a fan of the free market, the invisible hand, and inventing new markets, like Leadbeater's carbon trading (which I think is the *only* market based way to combat the natural drive of economic growth which depletes resources) as a means to further society's goals. BUT I think it only works if all the actors are acting rationally. I believe that when the is a 'market failure', the common theme is people not understanding the decisions they're being asked to make, and therefore acting irrationally. The current ills can all be linked back to people who made a decision without understanding the consequences down the line, discounting the future simply because they hadn't worked out what was likely to happen. When you build a derivatives market on these foundations, caveat emptor... Hence we had the dot com boom, where people didn't understand the underlying technology and what it could offer, we have had the credit bubble in the UK, where people were asked to take out loans they didn't understand, in particular credit card agreements where the punter didn't really know what an APR was but liked the look of the car they could buy, and in the US, even worse, we had poorly understood home loans compounded by a derivatives bubble. In this case I think the derivatives themselves were not inherently 'stupid', but the underlying loans were not understood by those who took them, and then each time they were sold on, the amount of information passed along with them decreased until the bankers/traders themselves did not know what they were buying, so that they were eventually also acting irrationally. The question is, how can you regulate/legislate for this once you know it's going to happen ? I believe the system will always create a bubble market if it can hide the real information about the product from an end user (as there is asymmetric information), so how do you ensure that the buyers have to understand. For instance, for the credit card, you could regulate that the consumer had to fill out a test question saying what they would owe in 2 years time if they didn't pay anything back. If no-one can answer it, the bank is not allowed to loan. For a CDO, you would have to be able to say how many underlying 'real' loan agreements there are and graph the demographic of the consumers (or something similar), maybe for a CDS you'd have to have fuller access to the accounts of the organisation beyond what the credit rating agencies are currently allowed. However what would you have done for the dot com stock boom, and what can you do for the next bubble, given that no-one knows what it is ? Can you really never 'regulate for stupidity' ? [i work in the private sector far from public policy, just an interested bystander]

-

Bbc News - House Price Falls At Fastest Ever.

camem' replied to Now or never's topic in House prices and the economy

prices crash from lows, not highs -

Some Further Analysis Of The Halifax Data

camem' replied to crown's topic in House prices and the economy

don't worry, they can have them with free skeletons -

Griptool wins. And the guy who said they would be on Wed not Thu. So any 'contacts' out there that know about the Halifax figures ? Perhaps Martin Ellis has other things on his mind by now ?

-

Oh good. I suppose that means I can feel all smug for not creating my hard earned dosh out of thin air.

-

Advisor said not to switch funds now as I'd be consolidating losses. On the bright side, I'm not old yet

-

To Those Who Say We Are Enjoying The Crisis

camem' replied to Nickolarge's topic in House prices and the economy

i wouldn't be so sure, i'm pretty sure he's in a growth industry. Stay well now. -

What Time Is The Second Bail Out Vote Completed?

camem' replied to markinspain's topic in House prices and the economy

That was the railroad vote methinks -

Let me know if the questions are too hard

-

Here's an update of the halifax/spreadfair graph. This plots house prices since 1983 (as from Halifax Seasonally Adjusted index) with a bit of data from the futures markets. A fixed 5.9% p.a. inflation is removed (by me) from index and futures so that everything is rebased to August 2008 money and so that the previous and current booms/busts can be compared And for homework : 1. Are house prices falling : A. more quickly than in the 90's B. not as quickly as the 90's C. consistently low inflation blah blah low unemployment blah blah gosh if the developers don't start building at a loss soon we might have to pull our fingers out and actually build some council housing blah blah did you know I've got a final salary pension ? 2. The recent falls are very consistent. Is this because : A. halifax were ahead of their time in defining their clever seasonal adjustment and the market has only just caught up, or B. this is about as fast as house prices can fall (with the low unemployment we are constantly reminded we have, anyway) ? C. you haven't seen anything yet. And for the rest of the marks : How far through the crash are we ?

-

The Inflation Adjusted Graph (1983-2008)

camem' replied to camem''s topic in House prices and the economy

It means what it looks like, house prices have a way to fall yet. The 'futures' are from a user to user betting site Spreadfair. The rest is from Halifax's house price index. Everything has been adjusted to today's prices by a single inflation factor to make the graph appear flat, however since this number has come out from several decades worth of house price data it should be pretty realistic in relation to house prices at least. Because of the inflation adjustment it tells you more about '% drop' and 'when' in terms of today's money than anything else - by the time we get to 2011, £130,000 of 2008 money will cost you more than £130,000 ! (how much more depends on other inflation measures I'm not even going to attempt) I don't have much control over the amount of 'pink' (I wish). In this case it is up to the spreadfair website. -

The Inflation Adjusted Graph (1983-2008)

camem' replied to camem''s topic in House prices and the economy

Feel free. The adjustment to futures prices that I've made is the same 5.9% p.a. (starting from July 2008). The 'raw' futures prices are at www.spreadfair.com. I think they're a good indicator for 'joe punter' sentiment, which is of course the bit of the market that keeps us all interested now the crash is beyond argument. The idea of the 5.9% is that it (by inspection) brings out the long term adjustment required to compare future house prices against past house prices (to make peaks=peaks, troughs=troughs). While this is of course simplistic, I think it gives a visually intuitive way to try and gauge how far through the crash we are. -

OK, here's an update of the seasonally adjusted halifax data since 1983 adjusted for long term 'house price inflation'. This turns out to be 5.9% p.a. to keep the peaks and the troughs aligned. I was all ready to say that it's all on track and we can tell exactly where, if not when it's going to bottom out if it's not different this time (around 130K in 2008 prices), but on this update the futures have overshot the historical troughs by some way (note they're inflation adjusted too) I've haven't bothered with the 2% graph on the basis that 2% doesn't seem to be relevant to anyone anymore (least of all BoE)

-

Was in the US last week - the radio adverts were interesting. After the advert for 'get a loan to make sure you don't fall foul of the recession' the next one was for someone who would buy your home 'whatever your foreclosure status' (as if everyone's got one), then one where 'oh my gosh you guys are great' actress realises that she can buy a home for less than her current rent. Fair enough you might say, but the quoted figure was $200 per month. To cover the mortgage on a house. Then there were plenty of adverts for foreclosed homes to buy on billboards around the place and at the airport on the way back the economist had 'the house price abyss' on the front cover with pic of a house falling into, well, an abyss. Tone of article was all 'when will it all end ? Not for ages' etc etc

-

All from today's letter :