Peter Hun

-

Posts

12,424 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Posts posted by Peter Hun

-

-

FFS, just build 50 nukes and have done with it. £250Bn is a drop in the ocean. Zero carbon emmissions, energy targets met, ans no ******ing windmills ruining our beautiful island.

Eco people can go ****** themselves.

Eco people would welcome building 50 new nuclear power stations, we haven't got 250billion to pay for it though. Wind power is cheaper, much cheaper if you take decommissioning cost into account.

Biggest wind turbine is now 10MW

This is the biggest Tidal energy generator being installed in the European Marine Energy Centre Tidal power test site in the Shetland Islands. Scotland has enough wind and tidal power potential to supply the whole of Europe, easily.

Only 1MW though

Atlantis Unveils AK1000 - World's Largest, Most Powerful Tidal Power Turbine

http://www.atlantisresourcescorporation.com/marine-power/technology-comparison.html

-

As Harry Monk was saying is this the same sort of calculation that said sticking a trivial amount of co2 into the atmosphere would have little/no effect?

You understand that man made production of C02 is not trivial? For instance 25liters of petrol burns to produce about 40Kg of CO2

Here's the wind energy stats for the current install base of UK wind power

http://www.bwea.com/ukwed/index.asp

5GW of wind power, replaces 5.8 million tonnes of CO2 per year, 136 thousand tonnes of sulphur dioxide and 40,000 tons of Nitrous Dioxide.

I did a calculation once; a life time of C02 from each person would take a storage tank the size of a small house. Anybody who produces it should be forced to buy and store the C02 for eternity, 'he who dealt it, owns it' after all. You would not need to worry about house prices, you would have a mortgage for the CO2 instead.

-

Down 90% perhaps, but it can still fall 100% from the current level.

Oh great, the whole of Spain would be for sale for 0 Euro's. I'll take the lot.

-

Nothing subtle like that...I mean they just don't add up!

Really?

They have probably been fabricated to hide the true extent of the falls. The Spanish are full into fake statistics.

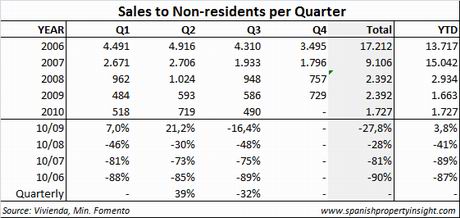

But you are right, the figures for 2008 and 2009 are identical, which is obviously a typo, 2008 total should say 3691.

-

Something odd with those numbers, look at the totals for 2008 and 2009.

The Spanish crash happen long before anywhere else. I think a lot of the 2007 sales were due to off plan purchases going through.

-

Edit: It's not on market for that price, it's a reserve.

disclosed reserve of €550,000 (plus VAT

People have a funny idea about reserve prices, they think it means something. It doesn't

-

I remember listening to that NPR podcast. The most concerning aspect was that many of those lots aren't even relics of this housing bust. Instead they hark back from either earlier booms in earlier decades or were simply investor traded speculative plots.

At least they are hurricane-proof.

-

The true extent of collapse in Spain

Holiday home sales down almost 90pc since 2006

Posted on December 17, 2010 by Mark

New figures from the Department of Housing reveal the true extent of the slump in holiday-home sales to foreigners

During Spain’s runaway housing boom of the last decade, tens of thousands of new homes were built on the coast with foreign buyers in mind. Unfortunately, foreign buyers didn’t show up to the party in expected numbers, which partly explain why Spain has such a glut of new homes on the coast.

But look how dramatically purchases of holiday-homes by foreigners have collapsed. Down 87pc in the first 9 months of the year compared to the same period in 2006, and -16pc Q3/Q2 At this rate foreigners buying holiday homes will do nothing to help absorb Spain’s glut of new homes. The figures are difficult to believe: Just 490 sales in 3 months over the summer. Are the figures wrong? If not, who will buy all those empty holiday-homes? Unemployed Spaniards?

http://www.spanishpropertyinsight.com/forums/viewtopic.php?f=2&t=5428

I know we have a sub forum for this, but I think its relevant to see the effect of the UK crash.

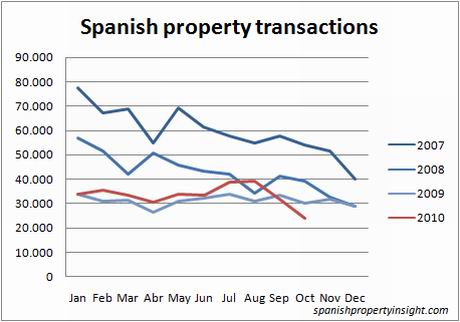

And the overall Spanish l market

Spanish property market down 20pc in October

'Only' down 75% since Jan 2007.

-

The European political elite has an abysmal grasp of international money markets.

They have done such a good job at convincing themselves, they cannot grasp how anyone would decline to buy their falsity just because their say so doesn't make it true.

If Ireland defaults it will take the rest of the EU banking system with it, including the Euro and the UK. US is also a possibility.

So there is no way they will allow it to happen, they will keep moving the bank debt to sovereigns until there is no where else for investors to invest and the problem goes away via inflation.

The Germans are going to be ultimately liable for the PIIGS debts, whether they like it or not.

IT may eventually get to the point where capital controls are introduced within the EU. Investors will be forced to invest in state bonds whether they like it or not.

Everyone claims its been great for Iceland, so maybe the Eurozone will be next.

-

The only difference this time is the size of debt owed in the debt bubble and in the early 90's I don't recall any major bank getting a bailout before house prices dropped. Clearly the BoE is correct in using what happened in the 90's to predict what will happen now.

+1

The low base rate is to protect the banks and allow them to recapitalise.

-

Am I missing something here? They're simply keeping a scaffolder and signwriter employed and reducing the prison population. True?

Its a picture from thirty years ago, right? itt looks like the southern states of the USA fifty years ago, with modernisation they execute their 'criminals' behind close doors, although if the Tea Party get in power their will probably state doing it in public again.

The US/Israel haven't invaded Iran becuase it would not be a military push over. I studied my engineering degree with an Iranian, he probably went into their missile industry, the two other English students went into the defence industry in the UK, tanks and torpedo's. With a developed economy (which it has) and western educated engineers and a focus there is no reason why their missile technology claims should be disbelieved (its often laughed at by western media).

In fact the 'Third world' should not be underestimated, some places like Africa will probably always be a basket case, however some countries will catch up to the West and are already there in some cases. Uruguay is now officially classified as first world, for example.

-

You know, Saudi Arabia went through this process in the early 1980's. Huge empty housing complexes. I don't know if they were ever used. I was told that they had such large surpluses at the time that there just wasn't anywhere to put the money safely, so they just built things. China going through the same process now?

Yes.

Chinese are desperate to find a place for their money, there was a detailed article about it but I've no chance of a link to it.

-

The USA still has massive coal and gas reserves. It can feed itself. Houses are reasonably priced. Petrol is cheap.

Britain is held hostage for its gas. It cannot feed itself. Houses are vastly overpriced. Petrol is extortinate.

I think the USA will be just fine. I'm not so sure about the UK.

Petrol is cheaper in the Uk than the USA. The difference is tax, which goes straight back into our pockets as opposed to profits for the oil producers.

-

Pretty much sums it up, well said. Just hope I'm not toast before I can reap the benefits of my gold stash.

Why do you keep telling the entire world you have a gold stash.

Don't you realise how easy it is to find out where you live and take it off you?

if the economy crashes like you are praying for, you can guarantee thats what will happen.

-

If the ultimate hard money is bullets, the US has the greatest reserves, no?

Nope, they have a shortage. They have been buying UK and israeli bullet stock piles due to lack of capacity in the USA. It takes an average of 150K bullets to kill each freedom fighter/insurgent, up from 35k in the Vietnam era.

-

I've just had a brand new boiler fitted in my 4 bed house, although I have a prepayment meter, EDF state on their web site that a key meter costs the same as a standard tariff, having said that, as a tight git i've been monitoring my gas usage since the new boiler went in and have adjusted the thermostat to( ball park)16 first thing for when i get up, 13 when i'm at work and 17 in the evening.

It's costing an average £4 a day, i'm quite able to afford this, having two lodgers to supplement all the bills, I have no mortgage and no debt, but if i were a family man with kids, mortgage, CC bills and so on, how the hell do these people manage with an average gas bill of over £100 a month on top of everything else?

A little snippet from Mumset, I think this young lady is in for a very nasty shock when they re-adjust her DD

AVeryMerryPersonalClown Tue 07-Dec-10 13:29:24

I'm scared that I'm going wrong somewhere!

3 bed house, gas central heating combi boiler, heating on constant due to stripping autistic boy and I pay £16 a month on DD.

* I think she meant Strapping

I live in Poland, in an apartment block. Unless it goes below -10c in the daytime I haven't switched on the heating. Well insulated these communist apartment blocks. I'm happy being at home all the time with a 20C temp.

-

Whats that now, 34 monthly surprises?

-

Wrong - once you give your 'money' (or more likely bank credit from another bank) to a bank, all you have is a credit from that bank. That's why it's called bank credit.

It's not the same thing as actually holding legal tender and the bank sure as hell isn't holding an amount of legal tender, equal to your credit, for you to withdraw.

Under normal circumstances you can treat the bank credit and money as the same thing. However, should the bank fail you will quickly find out the difference.

Bottom line is that you 'put money in a bank' at your own risk. You might hope that government guarantees pan out but I bet you that if a couple of the big UK banks had went under you'd have been waiting a very long time for your cash back (irrespective of the FSCS promises) and by the time you got it, it would be worth enough to buy a loaf of bread.

None of that actually contradicts what I said. A deposit in a bank is not a investment that returns a risk payment, it has to be returned on demand in the same form as deposited with a very fixed time scale. Now there can be delays in the process, but even Iceland upheld the depositors and in fact the UK government paid the depositors back very quickly.

That there can be problems doesn't deflect from the definition of a bank deposit.

The

-

Why not? CH4 powered cars could be the next boom waiting to happen. It will require a whole new infrastructure, everyone has to buy a new car, new ships and drilling rigs required; all planes to be converted or just scrapped and new ones bought. I can see the manufacturing boom already. Where do I sign up to ride the bubble?

What are you talking about you can buy gas in virtually every forecourt today and converting to LPG is pretty straightforward.

Very popular in Poland, LPG car sales out number petrol by a significant amount, like the Uk it works out les sthan half price

-

Japan's deflation in certain sectors (certainly not in things like food and fuel) will be over when the prices were allowed to fall to market clearing level. The Japanese just chose to do it over a long period of time (while Iceland decided to do it the quick ways).

Iceland still has many years of recession to look forward to and it will be paying for the default for a decade at least. there is no easy way out.

Regarding a slow crash in HPC, this is what a real 4% fall (3% inflation, 1% nominal falls in house prices) looks like over 8 years

-4.0%

-7.8%

-11.5%

-15.1%

-18.5%

-21.7%

-24.9%

-27.9%

Just remember that even tiny 1% annual fall makes for a big loss over the timescales we are looking at.

-

Only if you let it get to you.

Aye, Looking forward to saving and increasing my personal wealth. This gives me more time to invest in depressed assets before the next credit boom.

Western hydrocarbon-based industrial civilisation has peaked and is now set on a course of inexorable decline.I'm not certain the lack of oil will prevent the next boom (which is a change in stance from me), the abundance of fractured gas will compensate before alternatives take hold.

Limits on credit will drive the recession and that will take a ten year crash to pay down the debt overhang.

-

Peter Hun : The fundamental weakness in your arguments is that to accept them one must also accept that a privately held company and its shareholders can keep all the profits/benefits of success but put failure off on the backs of the general population. In this sense a bank is no different that any other private company. Now these types of businesses are supposed to be heavily regulated within the jurisdiction they are operating within, and this is the real protection for the those involved. But nonetheless they are still private businesses.

The logical extension of your assertions is that a private company can benefit 100% from success and not have any responsibility for their actions (including deserved imprisonment) if they fail.

Now by accepting this assertion here is the end game: The very institutions that have had their failures guaranteed are now reaping record bonuses and profits. This is possible because the government have assumed their liabilities (against the wishes of you and I, in the US the bailouts were opposed by the people 100:1). Now the ultimate insult is that our nations are becoming insolvent, but the banks are not. And as a result our nations (ie yours and mine) are now having to borrow from the very same institutions that have already failed.

Effectively the taxpayer, their children and grand children are being subjected to financial gang-rape by their politicians and the banking elite. There is simply no other way to look at it. We have a duty to resist this.

Whether you or I accept it, the governments have done so on our behalf. Banks are not limited liability private companies, no matter what they may claim, they are special entities and all countries accept that. Argentina tried the default route and found that one way or another they are going to have to pay back the debts and will pay a risk premium again in the future just for trying it on. Governments, and companies NEED to borrow money, don't ask me why, but they do; the interest rate will either cripple them or help them but ******ing over the lenders will only bite you and your grandchildren back.

However, thats completely irrelevant. This is depositors money.

The Icesave issue is not a case of Icesave dumping losses on the taxpayer, its a the icelandic government giving the loss to the taxpayer. A government is responsible for protecting bank depositors NO MATTER WHAT.

Depositors place their money in Icesave with the irremovable and immediate right to get them back in the currency they deposited them. Depositing money in a bank is not an investment, its a safe holding place, licensed and guaranteed by the central bank. If anyone doesn't understand that, then tough. Iceland's government understands that depositors should have complete safety and all depositors were protected (except for non-icelandic account holders, which is illegal..)

-

Someone has the balls to say it.

In an era where forecasts by permabears have gotten ample attention and vindication, few are as disturbing as this: a world recession until 2018.It comes from Eisuke Sakakibara, Japan’s former top currency official. He is known as “Mr. Yen” for his ability to move markets. Because Tokyo’s revolving-door politics often sends a new face to each Group of 20 meeting, he is one of the few Japanese constants in market circles. Traders may not know the latest finance minister’s name, but they know Sakakibara.

Japan is the master of muddling along, decade after decade, with little growth to show for it. And Sakakibara was a key player when Japan faced everything from the Asian crisis to Russia’s default to the onset of deflation to a banking collapse that saw the demise of Yamaichi Securities Co.

So, when an economist with Sakakibara’s background says “the world is set for a long-term structural slump reminiscent of the 1870s” when average global annual growth was about 1 percent, I can’t help but listen. The reason for the slowdown? Governments are putting fiscal austerity ahead of restoring stable growth.

Yes, there’s an eye-rolling quality to a former Finance Ministry mandarin giving economic advice. After all, officials there did Japan’s 126 million people a disservice by punting reform far down the road. They just borrowed and borrowed, leaving Japan with the largest public debt among industrialized nations and no exit strategy in sight.

Global Recession

Yet recent data in the U.S. and Japan and financial turbulence in Europe suggest a fresh global recession is a distinct possibility in 2011. If that happens, what levers are realistically available to revive demand? Interest rates are already at, or close to, zero. That leaves increased government spending as the only real way to stabilize things.

The trouble is, there’s little support for opening the fiscal floodgates in a meaningful way.

One reason is that there’s already loads of public debt out there. As of June, Japan’s $5 trillion economy had 904 trillion yen ($10.8 trillion) in debt outstanding. Too much debt is wreaking havoc in Europe, where Ireland was the latest domino to fall.

The U.S. is starting to rattle bondholders with its borrowing binge. President Barack Obama’s stimulus isn’t working the magic economists hoped. Neither is the Federal Reserve, as it goes the way of Japan with quantitative easing.

1937 Again

Worse, in the U.S. and other major economies, is the risk that it may be 1937 all over again. It was then that President Franklin Delano Roosevelt got stingy with stimulus, assuming that the Great Depression was over. The next year saw the economy in full retreat.

If Sakakibara is right, the global economy is in deep trouble. He envisions a broad slowdown that might drag on for seven to eight years. China can live a couple of years without U.S. and European growth, but eight?

To head it off, governments need to up spending. And, for the most part, they aren’t. Yet the U.S. can, and should, borrow more. To do that, it just needs to become a bit more Japanese, says Richard Duncan, author of the “The Corruption of Capitalism.”

There’s a single reason why Japan’s 10-year bond yields are below 1.3 percent and Asia’s No. 2 economy isn’t being downgraded. Since about 95 percent of Japan’s debt is held domestically, there’s no risk of capital flight. Japan borrows from its companies and people, an arrangement that’s roughly the mirror image of the U.S.

New, New Deal

That so many Treasuries are held in China and elsewhere makes the U.S. highly vulnerable. Duncan, chief economist at Blackhorse Asset Management Pte. in Singapore, says the U.S. needs another FDR-like New Deal to restore growth and competitiveness. Funding one means greater borrowing and the way to do it is by tapping private-sector cash, Japan-style.

Such suggestions are likely to fall with a mighty thud on Capitol Hill, which is moving in the opposite direction. Lawmakers calling for Ben Bernanke’s head forget why the Fed chairman is taking U.S. monetary policy into uncharted territory. It’s because Congress failed to pump enough money into the economy in the first place.

Japan is a cautionary tale. On the surface, the 4.5 percent annualized increase in third-quarter gross domestic product looked promising. The detail, however, showed that deflation is worsening no matter how many yen the Bank of Japan churns into the economy. This is anything but a typical recession, and world leaders are too distracted to see it.

In the U.S., the focus is on China’s currency. While a stronger yuan would be in the best interests of the global economy, it’s not the answer to all the U.S. problems. Japan is even more obsessed with exchange rates. And Europe is linearly focused on convincing investors that the euro zone won’t unravel.

In our time of currency fixation, perhaps a guy called Mr. Yen is the ideal messenger. Too bad his message is one of economic gloom as far as the eye can see. Perhaps even to 2018

-

BS

When the boomers had 'free education' in the 60s/70s/80s the top rates of tax were at various times 60, 83 even 98% (or 136% if you had investment income!). If they earnt big money they paid big taxes. Even the basic rate of tax for a time was 35%, almost as high as the 40% top rate for the period 1988-2008. I guess there was a small window between 1988 and 1998 when there were no tuition fees and no exhobiant income taxes, but for most boomers, that simply wasnt the case. These rates are far higher than would likely be proposed with a 'graduate tax'

House prices are a far bigger crime than tuition fees. No one forces you to go to uni, a house OTOH is pretty essential.

These selfish students just want capitalist rates of tax (ie none on them) with socialist levels of public services.

Good point. We live in a time of incredibly low income tax.

VAT has gone up a lot though. Started at 8% didn't? mind you vat is charged on optional crap to the biggest extent.

Pontin's Future In More Doubt As Developers Bid To Bulldoze Sites

in House prices and the economy

Posted