otherwayup

-

Posts

14 -

Joined

-

Last visited

About otherwayup

-

Rank

Newbie

")

-

Very, very nearly SNAP. Location - Essex

-

That's hardly illiquid either, unless you are prepared to take a massive hit and walk away halfway through.

-

Please tell me where can I get this sort on NET interest?

-

Does Your Mp Receive Rental Income?

otherwayup replied to Democorruptcy's topic in House prices and the economy

Listed in the Update History John Baron - Billericay Updated 13 March 2007 8. Land and Property Removed - Two residential properties in London from which rental income is received. Added - Three residential properties in London from which rental income is received. -

Off Topic but, KingCharles1st , I assume this has been asked before. Please post link to full size image of your Avatar. Ta.

-

My Very First 'black Day' Thread

otherwayup replied to shedfish's topic in House prices and the economy

I hope not. The Postal strike has delayed delivery of my "bank the recent rises and stick it in a fixed interest fund" pension transfer form. Six months ago, the last 5 or 10yrs might as well have not happened. I hope it all holds up for another week or two. -

Thanks guys.

-

She had a little trouble passing the tube through the hole in the second section of wall, and that was with a cut-away demo wall where she could 'see' the second hole. Good luck doing it blind!

-

Just read something on the HSBC site that has made me think. I opened a cash ISA last tax year with HSBC and the initial deposit money is still in the ISA account. I haven't added any money since initial deposit last tax year. I had assumed I could open a new cash ISA this tax year with any other provider, but the HSBC wording implies not so and that I cannot use another provider if the ISA I opened last year is still going. Is that right and I cannot use someone else this year?

-

I've done my bit. BBC: Have we bottomed yet?

-

If you are 'investing', I would be wary of ETCs at the moment (see http://www.housepricecrash.co.uk/forum/ind...t&p=1805745 ). Short term trading is less affected, obviously.

-

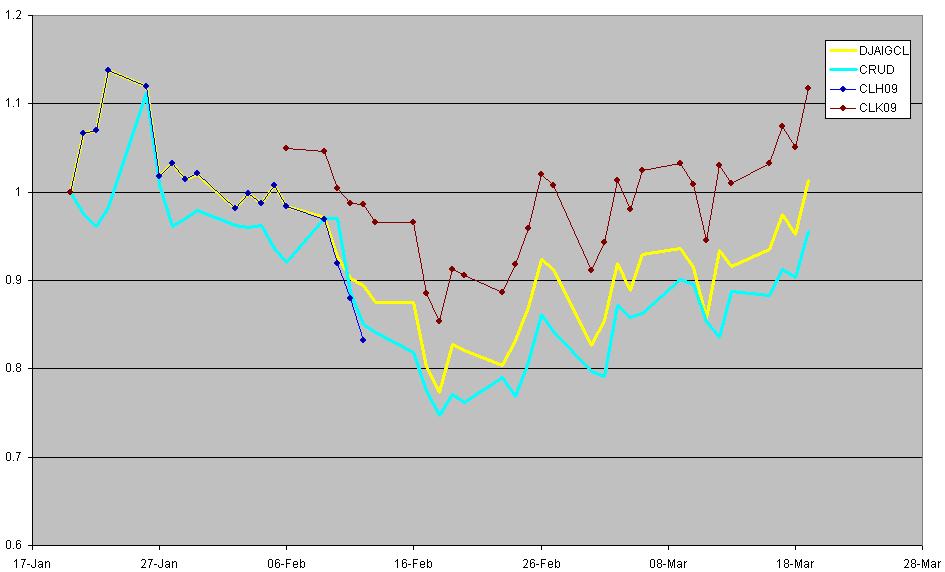

I disagree. For example, the ETC CRUD attempts to track an index (DJAIGCL). This index tracks the daily % change of WTI Crude Oil future(s). Notice it's the 'change', not the absolute price. Every two months, the index switches over (rolls) to a later contract. If I have attached the graph correctly, you sould be able to see that the index follows the ups and downs of the futures contracts accurately, but not the absolute price of the contracts. The roll occurs between 6th-12th Feb. All prices rebased to 1 at start date of 20th Jan. In this example from 20th Jan to 19th March, the contract price being followed increases nearly 12%, whilst the index and ETC values are much lower (the ETC has actually lost nearly 5%). This difference in value is due to Contango (later contract price being higher than near contract price) and has severly affected commodity trading in recent months. (p.s. I learnt all this the hard way :angry: )

-

Any reason why you didn't go for SC24 (same expiry date), which the simulator says would return 98% at 4000?Ignore this question, I just noticed the date in the simulator kept resetting to today even though I thought I'd selected 12th Feb. Must remember to watch out for that.

-

Just Listened To An Excellant Programme On Radio 4

otherwayup replied to rainbow's topic in House prices and the economy

How about "Nail em out"